Despite the long list of what you can’t do with retirement assets, there’s an exception that lets you use all or part of your retirement funds to start, buy, or grow a business without incurring tax penalties. The IRS calls this arrangement Rollovers for Business Startup (ROBS). ROBS is a legal way for people to leverage their pre-tax retirement funds to start a business.

Note: ROBS is also often called 401(k) Business Financing, as it most commonly leverages the funds from a 401(k) plan — though more retirement plans than just 401(k) plans are eligible.

However, just like there are prohibited transactions for personal retirement plans, there are prohibited transactions in ROBS.

What is a Prohibited Transaction?

A prohibited transaction in the context of retirement plans refers to the use of retirement funds for purposes that don’t meet the criteria set forth by the Internal Revenue Service (IRS).

Despite the long list of what you can’t do with retirement assets, there’s an exception that lets you use all or part of your retirement funds to start, buy, or grow a business without incurring tax penalties. The IRS calls this arrangement Rollovers for Business Start-up (ROBS). ROBS is a legal way for people to leverage their pre-tax retirement funds to start a business.

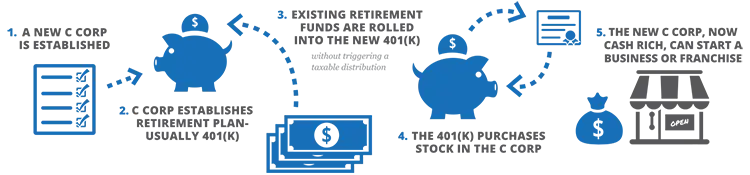

What are Rollovers as Business Startups (ROBS)?

Rollovers as Business Startups (ROBS) gives aspiring business owners access to their pre-tax retirement funds to start, buy, or grow a small business. The major benefit is that ROBS won’t trigger early withdrawal fees or tax penalties when set up correctly. ROBS uses the “qualifying employer securities” (QES) exception under the Internal Revenue Code section 4975(d)(13). This allows you to use your retirement funds to invest in a privately held C corporation that can then purchase a small business.

Why is ROBS Exempt from Prohibited Transaction Rules?

The Employee Retirement Income Security Act of 1974 (ERISA) was designed to encourage employees to take control of the direction of their retirement funds. ERISA allows for the use of QES that lets you leverage your qualifying retirement funds to start, buy, or grow a small business or franchise. The rules within ERISA also exempt ROBS from prohibited transaction rules.

- ERISA § 406 sets forth the general prohibitions against a prohibited transaction (sale, exchange, loan, services, etc., of plan assets to a party in interest). The parallel provisions are in IRC § 4975(c)(1).

- ERISA § 408(e) provides an exemption of the prohibited transaction rules for “qualifying employer securities” if three conditions are met:

- The sale is for adequate consideration.

- No commission is charged with respect to the sale.

- The plan must be an “eligible individual account plan.”

The parallel exemption in the Internal Revenue Code for qualifying employer securities is IRC § 4975(d)(13).

- The term “eligible individual account plan” is defined in ERISA § 407(d)(3)(A) as one of several listed types of pension plans, and one of the listed categories is a “profit-sharing” plan.

- A 401(k) is a type of profit‐sharing plan. Guidant’s 401(k) plan contains the requisite authority required by ERISA § 407(d)(3)(B) for the trustee to acquire and hold QES in excess of the 10% limit under ERISA § 407(a)(2).

- The 10% limit on a plan’s acquisition of qualifying employer securities does not apply to an “eligible individual account plan” according to ERISA § 407(b)(1).

How to Avoid ROBS Prohibited Transactions

ROBS prohibited transactions are the activities that can void the ROBS arrangement. It’s important to understand the requirements that must be met for the ROBS structure to maintain its tax penalty-free status. We call these the “five pillars of ROBS.”

- Client’s Duty of Prudent Investment

As a trustee and fiduciary of the retirement plan, this individual must act in the retirement plan’s best interest.

- Adequate Consideration for Fair Market Value

The plan cannot pay more than Fair Market Value (FMV) for the stock it purchases in the C corporation.

- The Corporation is an Operating Company

The business must be an active, operating company, not a passive investment like real estate property.

- Employer Must Not Discriminate Against Non-Highly Compensated Employees

The employer must offer each employee the ability to purchase stock in the company with their retirement funds.

- All Rollover Participants Must Be Bona Fide Employees

The individual(s) who completes the 401(k) rollover must also be a bona fide employee of the business they start or purchase, providing an actual service to the business.

The Most Common ROBS Prohibited Transactions

These are the most common actions that can trigger a prohibited transaction. They are fairly simple to avoid – especially when you work with an experienced ROBS provider who can help you set up, maintain, and keep your business’s 401(k) plan in compliance with the IRS and DOL.

Excessive Owner Compensation

If you use your retirement funds to invest in a C corporation, you must be a “bona fide employee of the business.” There aren’t any requirements around what work tasks you have to perform to be considered a bona fide employee: you can handle administrative work or act as the company’s CEO. Whatever work you do, you are entitled to be compensated for this work. You just need to keep in mind that trouble can arise if the pay you take is above the normal value of the duties performed or the salary comes directly from the ROBS transaction funds.

As a fiduciary of your retirement plan, the rule is that you must always act in the plan’s best interest. An inflated salary or taking compensation directly from the ROBS proceeds can be a red flag to the IRS that you’re trying to take advantage of the retirement fund – which could trigger a prohibited transaction. You should ensure your salary amount is in line with reasonable market standards.

Personal Use of Business Property

As the business owner, you can’t use any of the business property for personal use. This includes your spouse and immediate family.

Using Plan Proceeds to Pay Promoter Fees

The ROBS structure can be complex to set up and maintain. You will likely want to work with an experienced ROBS provider to ensure the business is compliant with the rules and regulations set forth by the IRS and DOL.

Many ROBS providers charge an initial fee for setting up the structure and ongoing fees to properly maintain the retirement plan. The IRS calls these “promoter fees” or “professional fees.” Using funds from the ROBS transaction to pay these promoter fees might trigger a prohibited transaction, as a fiduciary can’t use funds from the retirement plan in his or her best interest. To avoid this prohibited transaction, most ROBS providers require business owners to pay their fees out of pocket.

Rely on the Experts

ROBS can be a great solution for aspiring business owners who don’t have enough cash on hand to start a business or just don’t want to take on debt with a business loan. But since the rules surrounding the ROBS structure can be complex, it’s important to work with an experienced ROBS provider like Guidant that can help ensure your corporation and its retirement plan are set on a strong foundation.

Get started funding your business by contacting a Guidant representative with the form below.